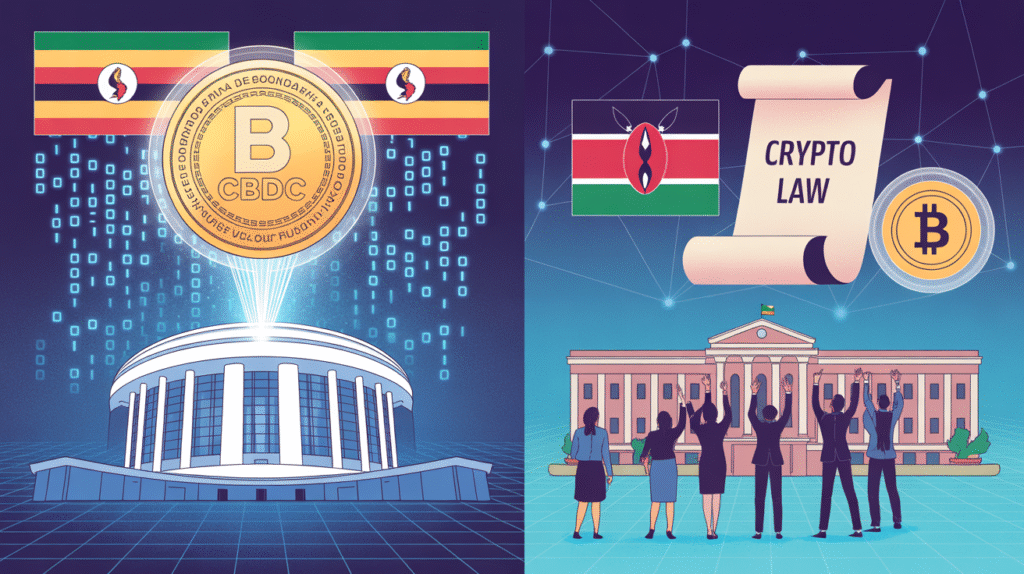

Uganda’s digital shilling is now live on a permissioned blockchain developed by the Global Settlement Network (GSN) in partnership with Diacente Group. This isn’t a wild experiment: it’s backed by Ugandan treasury bonds to ground it in real asset value.

The access runs through your smartphone, provided you clear KYC (Know Your Customer) and anti-money laundering checks. The pilot also ties into a broader “tokenization” vision: converting real-world assets like solar farms, mining projects, or agricultural hubs into digital tokens.

Why Is This Step Significant?

Uganda is trying to build a transparent, scalable infrastructure that can attract investors while protecting against fraud and misuse. Edgar Agaba of Diacente puts it well: “We’re integrating tokenization and CBDCs into Uganda’s roadmap to unlock value, empower industries, and drive inclusive growth.”

Kenya’s Turning Point: Crypto Bill Nears Law

Kenya’s legislative body has passed a bill that would regulate Virtual Asset Service Providers (VASPs)- exchanges, wallets, token issuers, and more. The bill now awaits President William Ruto’s signature.

Under the bill, the Central Bank of Kenya will handle payment and custody aspects. Meanwhile, the Capital Markets Authority will govern trading and investment functions. The law includes KYC/AML mandates, rules against misleading ads, and fines for violations.

If signed, this sets a clear compliance regime for crypto businesses- something many have called for. Until now, crypto in Kenya operated in a grey zone. This new law draws lines: who must register, how systems should work, and under what penalties.

Why These Moves Matter

1. Balancing Innovation with Control

CBDCs and tokenization are exciting. But regulators must not let them become tools for money laundering. Uganda’s pilot embeds AML protocols from day one. Kenya’s bill similarly builds compliance into its core. These acts show the balance many nations now seek: enabling innovation while preserving control and safety.

2. Creating Trust in Digital Systems

Money is trust. You won’t accept a digital currency unless you believe it’s secure, governed, credible. Uganda’s use of treasury bonds helps anchor the digital shilling in tangible value. Kenya’s law, with strict rules and oversight, aims to bring legitimacy to crypto platforms.

3. Cross-border and Regional Effects

These moves also reflect broader signals across Africa. Crypto adoption in Sub-Saharan Africa is among the highest globally. As countries adopt regulation or CBDCs, others will feel pressure to follow or align.

A citizen or business in East Africa should now watch not only national developments but also regional compliance trends, interoperability, and harmonization of standards.

Caution Points and Challenges

-

Permissioned vs. Permissionless

Uganda’s CBDC is permissioned-users and nodes are controlled. That’s safer but less open. It raises questions: who sets permissions? Who audits them? -

Data Privacy and Surveillance Risk

A state that controls the digital ledger can also monitor transactions closely. Without strict protections, CBDCs can become tools of surveillance. -

Implementation and Liquidity

Even a well-designed CBDC needs broad user adoption, system reliability, and liquidity channels. Tokenization of assets also requires regulatory, legal, and valuation consistency. -

Regulatory Uncertainty

Kenya’s bill is still pending signature. Until enacted, ambiguities remain: how old laws intersect, how enforcement will play out, how international crypto firms will adapt.

What Stakeholders Must Watch

-

Crypto Platforms & Exchanges: Start mapping compliance to Kenya’s expected standards. For Uganda and similar markets, consider how tokenization and CBDC integration might demand new business models.

-

Investors: Digital assets anchored by real assets (through tokenization) may gain premium appeal. But assess regulatory risk, especially in jurisdictions under legislative flux.

-

Regulators & Policymakers: African countries observing these experiments can learn. Uganda’s tokenization + CBDC offers a real testbed. Kenya’s VASP regulation may provide a blueprint for others.

-

Citizens & SMEs: These changes aren’t just technical. They affect how people pay, save, trade assets, and engage with finance. Education and user experience will be major barriers.

A Turning Tide in African Digital Finance

With Uganda’s CBDC pilot live and Kenya’s crypto law poised to take effect, East Africa is becoming a frontline in the digital money revolution. These efforts reflect a new maturity- where ambition meets accountability.

Yes, challenges remain: enforcement, user adoption, privacy, regional harmonization. But each step:the tokenization of real economy assets, or a formal crypto licensing regime, moves the region toward systems with stronger governance.

Digital money is no longer just about tech. It’s about trust, law, and how power flows in societies. Africa’s next financial era will be shaped by how smartly nations manage that balance.